President Trump has used Twitter as a platform to criticize and insult a number of people and entities, including Rosie O'Donnell, Nordstrom's, Canada, the NFL, Puerto Rico, Robert DeNiro, the NSA, Mark Cuban, and Chicago. Shortly before Christmas, he decided

to rip on the Federal Reserve (see below).

I will pass over the irony of Trump not being capable of understanding

trade wars or a

strong dollar. What I would like to cover is Trump's animus towards the Federal Reserve. Trump's tweet was in response to the Federal Reserve (the Fed) raising interest rates again. On December 19, the Fed

raised the interest rate from 2.25% to 2.5%, resulting in the fourth interest rate hike this year.

When discussing interest rates here, we are referring to the federal funds rate, which

is the rate at which "depository institutions, i.e., banks, lend reserve balances to other banks on an overnight basis." The federal funds rate is by far the most influential interest rate because it affects how individual consumers spend and save, as well as businesses.

On the one hand, raising the federal funds rate makes it more expensive to borrow money. This would mean that buying a home became more expensive (although selling one became more lucrative). It also makes it more expensive to pay off debt, which is disconcerting given the trajectory of government debt. On the other hand, raising the federal funds rate incentivizes saving. The Fed is looking at its

dual mandate, which essentially to keep inflation at around 2 percent and unemployment at around the natural rate (estimated at

4.6 percent). Since inflation is projected to get higher and we are near full employment, the Fed wants to take its foot off the break

because demand is growing faster than supply. The Fed's mentality is that it is better to ease up on the gas pedal than it is to overheat the economy and slam right into a recession. To better understand why the Fed would want to make borrowing more expensive, it would also help to explain the neutral interest rate.

Neutral Interest Rate

As these primers from the

Brookings Institution and the

Dallas Federal Reserve explain, a neutral interest rate is the estimated rate in which investment in the economy is equal to the amount of capital or savings. This is the magic amount just high enough at which savers can save and just low enough where borrowers feel that borrowing money is not too expensive. The neutral interest rate is neither too accommodating nor too restrictive. Part of what makes this difficult to calculate is that the neutral interest rate is in fluctuation (see below). This dynamic rate takes into account multiple factors, including productivity growth, demographics (e.g., aging population), and fiscal stimulus (e.g.,

Roberts, 2018).

Reasons to Raise the Interest Rate

Some basic economic fundamentals

dictate that we should raise the interest rate. Employment is really high. Normally, a lower interest is used to incentivize businesses to invest, thereby generating greater employment. Now that we are not in a recession, we do not need the easy money anymore. Plus, the GDP and wage growth have been growing in 2018, even amidst the interest rate increases.

There are some other

wonderful benefits. Banks are more likely to lend money, which is good since lending practically came to a halt during the Great Recession. Getting off of quantitative easing also means that the stock market can react more to economic fundamentals and less to whether the Fed will perpetually support an expansionary monetary policy. It also means that bonds and bank accounts

will have higher yields. A higher interest rate is also anticipated to lead to a stronger dollar,

which is good if you're an American looking to invest internationally or travel abroad, a foreign company with American holdings, or a foreign company with exports because your exports are perceived as cheaper relative to American products. The reverse is true for foreign consumers, American producers, or American companies with lots of business abroad.

Another factor to consider

is optics. The Fed maintains its reputation in part by maintaining its independence from the White House. If Trump is perceived to be pulling the strings of the Fed, it's bad for business, and ultimately, the global economy.

Reasons Not to Raise the Interest Rate

Raising the interest rate has some drawbacks. Consumers will

have to pay more on their loans, which means less money for spending or saving. Given the lack of propensity to save in the U.S. in the past half century, a higher interest rate might not result in a higher savings rate. On the entrepreneurial level, it makes it more expensive for businesses to pay off debt, which means that businesses are less likely to make new investments. Debt servicing also has the potential to reduce employees' wages. Higher interest rates

create issues with government debt and the increased cost of government borrowing. Those who are against raising the interest rate

point out the fact that inflation has generally remained below the Fed's targeted 2%, and has declined in recent years. Based on this argument, there is

not much need to raise the interest rates if inflation is this low. Matthew Yglesias also

makes the argument that the economy might not be as strong as it seems, mainly because labor force participation is lower than the official unemployment rate signals.

Postscript

Adjusting the interest rate acts as a reminder that every form of public policy has its tradeoffs, including monetary policy (see tradeoff on a strong dollar

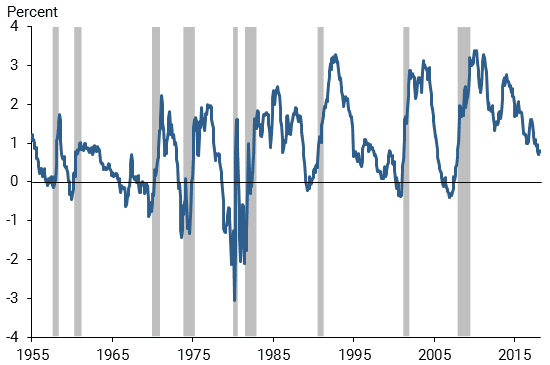

here as an example). It is also a reminder of how elusive predicting the economic future can be, even for the experts. Current Fed estimates of the neutral rate

are somewhere between 2.5% and 3.5% (see Fed figures

here). This would mean that the current interest rate is at the low bound of the neutral rate estimate. Based on these estimates, we are now within range. I do worry about the pace at which the interest rates are increasing since too fast of an increase could cause some unintended reactions in the stock market or the housing market.

At the same time, these rate increases are increasing at more modest quarter of a percent. I do believe, much

in accordance with the chairman of J.P. Morgan Chase International, that now is a good time to normalize the interest rate since the inflation rate is at the Fed's target, economic growth is good, and unemployment is low (also see Cato Institute

policy brief about normalizing monetary policy). I don't have a crystal ball, but I would guess that given current economic strength (not to mention the stock market's

recovery yesterday), the increase from 2.25% to 2.5% isn't going to be as dire to the U.S. economy as some suggest.