First, a brief explanation of an interest rate. The interest rate is the amount, either in percentage or dollar amount, charged by a lender to a borrower for the use of their assets. Essentially, it is the cost of borrowing money. There are multiple factors that go into account for the interest rate, whether that be for a loan on a house, on stocks, and on bonds. One of the factors is that of time, and this is where the yield curve comes in. Typically, a ten-year Treasury bond has a higher interest rate than a two-year Treasury bond to compensate the lender for the time difference. The difference between the two interest rates is referred to as the "spread." A positive spread means that the interest rate for the ten-year bond is higher than that of the two-year bond. The normal spread will take the shape of an upward-sloping yield curve, as is depicted below.

That is what happens with a normal yield curve. That is not always the case. Sometimes, there are moments when the short-term bonds have higher interest rates than long-term bonds. This moment is referred to as an inverted yield curve. What an environment with a negative spread would mean is less profitability for banks. While you might not necessarily care about banks or the U.S. Treasury, this has investors spooked.

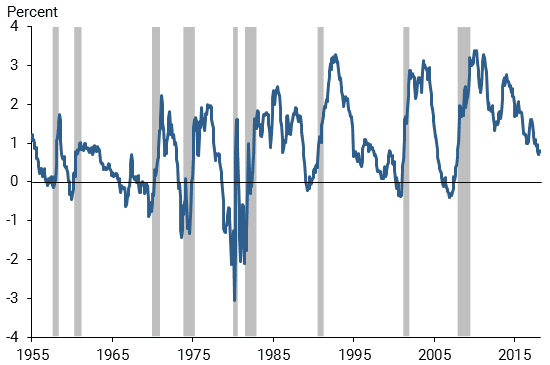

Likelihood of a Recession

This is particularly irksome for investors because an inverted yield curve is related towards higher risk of a recession. How much higher exactly? A 2018 economic paper from the Federal Reserve Bank of San Francisco (FRBSF) points out a scary fact: every recession in the past 60 years was preceded by an inverted yield curve. This trend is not only true in the United States, but in other developed nations. The FRBSF goes as far as calling the yield curve "one of the most reliable predictors of future economic activity."

There are a couple of things worth noting. The first is that FRBSF found that the recessions take place six to twenty-four months after the yield curve inverts. Assuming 100 percent accuracy, that means we could have until the end of 2020 before the United States experiences a recession. The Federal Reserve Bank of Cleveland (FRBC) indicates in its analysis that there were two false positives: one inversion in late 1966 and one flat yield curve in late 1998. This would imply that treating the yield curve as infallible is not accurate.

The FRBC is also hesitant on using the yield curve as a predictor for two reasons. The first is that the probability itself is subject to error. The second is that yield curves do not function in the same way as they did in the past, and that is due to different underlying determinants. For example, yield curves have historically been brought on by tight monetary policy. Right now, we have lower interest rates than the historic average, so that case is hard to make. The quantitative easing has distorted the long end of the yield curve. To adjust for it, the Federal Reserve came up with the alternative measurement of the "near-term forward spread," which seems to have better predictive power. Fortunately, this spread has not indicated a recession as of yet. Also, the spread between three-month and ten-year bonds is a more accurate predictor than with the two-year-bonds, and fortunately, there has not been an inversion between three-month and ten-year bonds.

Conclusion

Historic data suggest that a recession is coming soon. Even if we were to set aside the yield curve, we could be worried about contagion from Italy's budgetary woes or the Brexit. We could be worried about Trump's trade policy or the Fed's monetary policy. On the other hand, there are multiple positive economic indicators, including GDP growth, low unemployment, and high consumer confidence. We could fret over the fact we're in the longest bull market in history by saying "we're due for another recession" or we could learn how to keep the bull market going for even longer. I do worry about a recession because a) economies have booms and busts, and b) we have indicators in the global economy that could derail the bull market. At the same time, I am not quite ready to say that this yield curve inversion signals an imminent recession. Even the Federal Reserve of New York predicts an 11 percent chance of a recession in the next year. At this juncture, I will take a "wait and let's see" approach to see what happens within the next year.

No comments:

Post a Comment